Personal Umbrella Policies: What You Need To Know

A Personal Umbrella policy is the best and least expensive way to purchase high limits of liability protection. However, this is one of the least understood policies by the public.

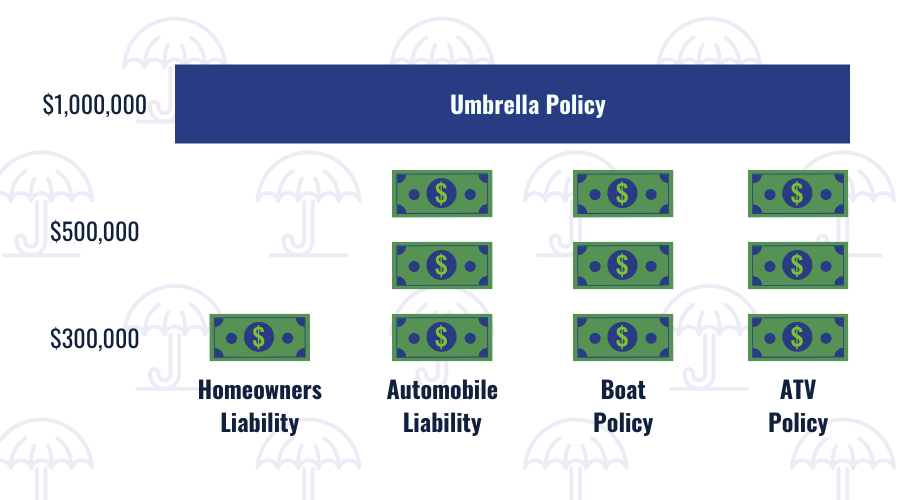

What Does an Umbrella Policy Cover?

An umbrella is a liability policy; and it is an excess liability policy. That means that it provides you with liability coverage in excess of the protection you have from another liability policy. We call the other policies the “underlying” coverage. Here is how it works…

Here, the insured has a Homeowners Policy with a liability limit of $300,000, a Personal Automobile Policy with liability limits of $500,000, a Boat Policy with liability limits of $500,000, and an ATV Policy for a quad with liability limits of $500,000. Then the insured has an Umbrella Policy with a limit of $1,000,000.

If the insured is involved in an automobile accident and a lawsuit is filed against the insured, the total coverage provided for the accident is $1,500,000 with the first $500,000 of limit coming from the Automobile Policy and the next $1,000,000 of limit coming from the Umbrella Policy. An Umbrella Policy does not provide coverage for judgements or settlements against the insured until the underlying policy limits have been exhausted.

The Underlying Policies

Each insurance company will have their own guidelines for the minimum limits that the insured must have on the underlying policies to be eligible to purchase an Umbrella Policy. There are two approaches that we see in these policies to address maintenance of the underlying limits.

Blanket Limits Approach

In these policies, the policy language outlines the minimum limits that you must have on the underlying policies without specifically naming your individual policies.

Named Underlying Policy Approach

In these policies, the insurance agreement specifically names the policy to which the Umbrella Policy attaches as an underlying policy. These policies also list the minimum limits that you must have for each type of policy.

What Happens If You Don’t Maintain the Underlying Policy?

If you do not maintain the underlying policy, there is a penalty. If you drop the coverage altogether, the penalty could be the imposition of a retention (deductible) of the required minimum limit outlined in the policy or the elimination of coverage under the umbrella for that exposure. Either of these penalties is quite severe.

If you maintain the coverage, but do not have the limit required or specifically named in the policy, the policy may eliminate umbrella coverage until the required limits have been met. This is the creation of a deductible.

For example, if the insured renews their boat policy with a $300,000 limit rather than the required and named limit of $500,000 and then has a loss – the Umbrella Policy will not start coverage until the full required limit has been paid out. Here, that creates a $200,000 deductible for the insured before the Umbrella Policy will address the claim.

Expand Your Personal Coverage

It’s important that you have the right amount of coverage for your personal lines of insurance. Without it, you can see yourself spending out of pocket, which could cause debt or other situations you’d rather avoid. For this reason, we hope you will consider a Personal Umbrella policy.

Contact us for more information or to move forward with this type of policy.